Published May 2, 2025

Why Today's Foreclosure Stats Aren’t What You Think

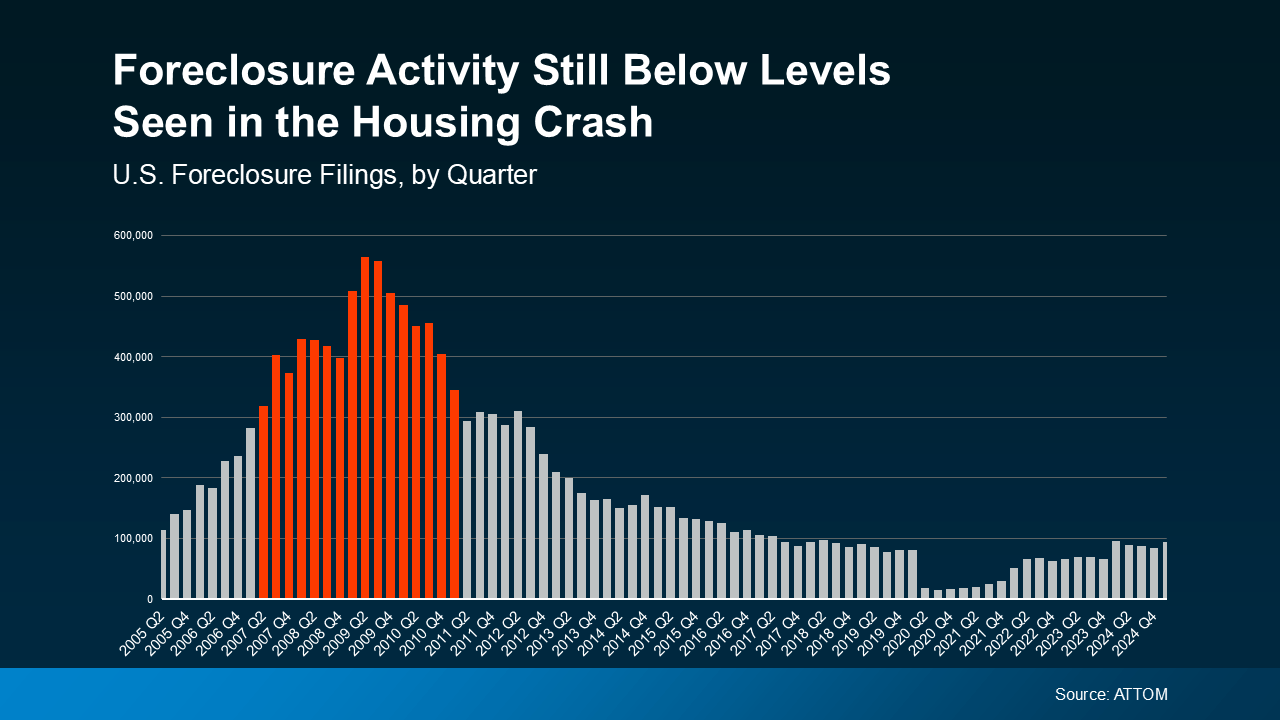

When prices are climbing on just about everything—from groceries to gas—it’s natural to feel uneasy about what that might mean for real estate. If you’ve seen recent headlines about rising foreclosure numbers, you might be wondering: Is this the beginning of another housing crash?

Let’s take a step back and look at the full picture—because the truth is, today’s foreclosure numbers tell a completely different story than they did in 2008.

A Quick Reality Check: This Isn’t 2008 All Over Again

Yes, foreclosure filings have increased slightly in the latest report from ATTOM. But in context, those numbers are still well below historic norms—and nowhere near the spike we experienced during the last housing crisis.

Back then, risky loan practices left many homeowners with unaffordable payments. The result was a wave of foreclosures, a flooded housing market, and rapidly falling home values.

Today, the situation is much different.

Lending standards are stricter. Buyers are better qualified. And most importantly, homeowners have something many didn’t back in 2008: equity.

The Hidden Safety Net: Homeowner Equity

Even when life throws financial curveballs, today’s homeowners often have a strong safety net—built by rising home values over the past several years.

Rob Barber, CEO of ATTOM, explains it well:

“Strong home equity positions in many markets continue to help buffer against a more significant spike [in foreclosures].”

In other words, homeowners who face hardship can often sell their homes and avoid foreclosure entirely. That’s a major contrast to the situation in 2008, when many owed more than their homes were worth.

Rick Sharga, CEO of CJ Patrick Company, emphasizes the point:

“Homeowners—including those in foreclosure—possess an unprecedented amount of home equity.”

Perspective Matters: Don’t Compare Today to 2020

It’s easy to look back at the extremely low foreclosure numbers of 2020 and 2021 and feel alarmed by any increase. But those years were an anomaly. A nationwide foreclosure moratorium was in place to help people through the pandemic—artificially lowering foreclosure numbers during that time.

If we compare today’s market to more typical years like 2017 through 2019, the current number of filings is actually below average.

Yes, Foreclosures Are Emotional—But This Isn’t a Market Crisis

Foreclosures are personal and painful. Behind every statistic is a family facing a tough moment, and that matters.

But from a market-wide standpoint, this is not a sign of systemic trouble. It’s a reflection of a market adjusting, not collapsing.

Bottom Line: There’s No Need to Panic

The small increase in foreclosure filings is worth noting—but it’s not cause for alarm. Most homeowners today are in a much stronger financial position, with high levels of equity and far more resources to navigate challenges.

See What A.I. Can Do for Your Home Sale

I’m one of the few A.I. Certified Agents in the world—and the only one in Summit County.

That means I use advanced, cutting-edge marketing strategies that traditional agents don’t even know exist. From real-time market analytics to targeted digital exposure, I bring tools to the table that give my clients a serious advantage.

If you’re thinking about selling your second home in Breckenridge—or just curious about your home’s value—let’s have a conversation. I’ll walk you through your options, no pressure, no obligation.

Call: (970) 390-3711

Email: kim@kimobert.com

Website: kimobert.com

Let’s explore what’s possible—on your timeline, and on your terms.

|

or another way