Published April 22, 2025

How To Stay Grounded When Mortgage Rates Keep Shifting

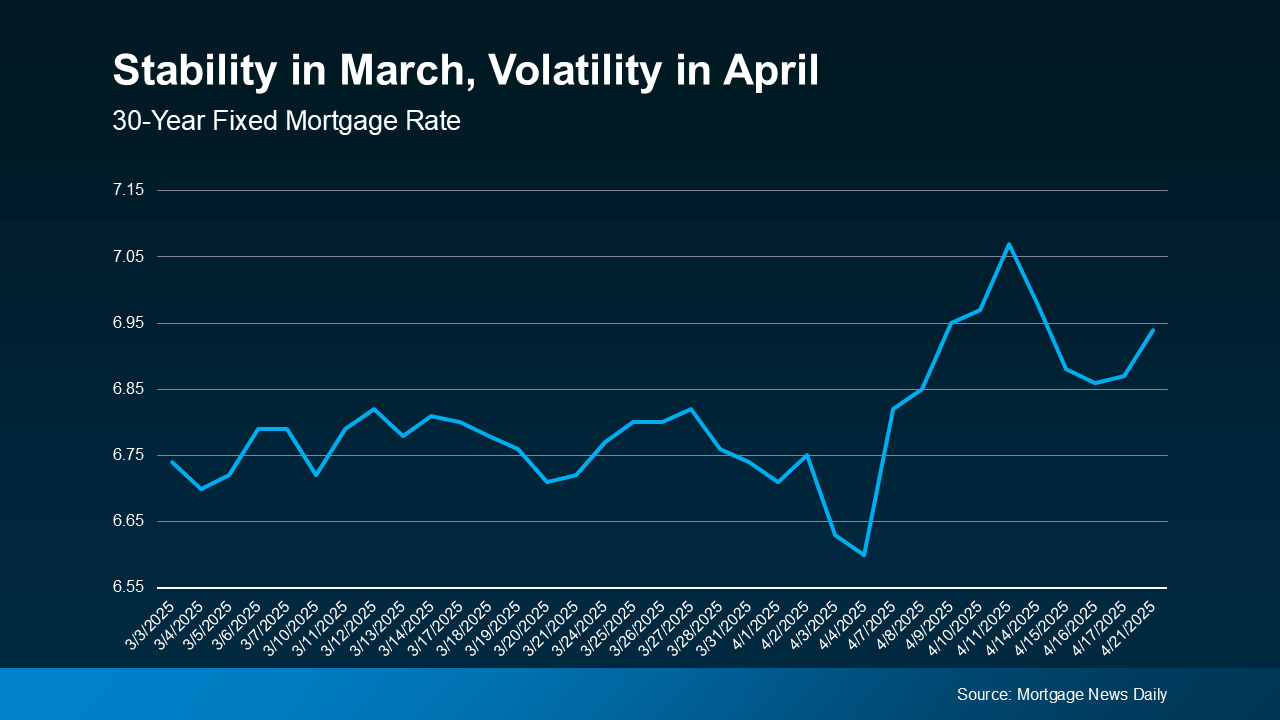

Have you noticed how unpredictable mortgage rates have been lately?

One day they dip just enough to make you hopeful. The next, they bounce back up like nothing happened. For anyone considering buying—or selling—a home, this back-and-forth can feel like trying to catch snowflakes in the wind: beautiful, fleeting, and frustrating.

Just take a glance at the trends this April. After a relatively steady March, mortgage rates decided to throw us all a curveball. That kind of volatility usually happens when the economy is in transition. So if you're sitting there wondering if this is the right moment to buy your next property—or sell the one you're barely using—you're definitely not alone.

Here’s the truth: timing the market perfectly is nearly impossible. But that doesn't mean you're stuck waiting and worrying. Instead, let's focus on what you can control.

1. Polish Your Credit Score

Think of your credit score like your passport to better mortgage rates. Even a modest boost can mean a noticeable difference in your monthly payments. As Bankrate puts it:

“Your credit score is one of the most important factors lenders consider… The higher your score, the lower the interest rates and better terms you’ll qualify for.”

If your score needs some improvement, now is a great time to chat with a loan officer you trust. They can help you figure out where you stand and how to improve it—so you’re ready when the right opportunity comes along.

2. Explore Different Loan Types

You’ve probably heard of conventional loans, but what about FHA, USDA, or VA loans? Each one has its own structure and benefits. According to the Consumer Financial Protection Bureau:

“Rates can be significantly different depending on what loan type you choose.”

The key takeaway? Not all mortgages are created equal. It’s worth having a conversation with multiple lenders to discover what works best for you and your long-term financial goals.

3. Think About Your Loan Term

Just like there are different types of loans, you also get to choose how long you’ll repay them. Whether it’s a 15-year, 20-year, or 30-year term, your decision will affect your interest rate, monthly payment, and how much you pay in interest over time.

Freddie Mac puts it this way:

“Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay…”

A trusted loan officer can help you compare different terms and decide what makes the most sense based on your goals and timeline.

Bottom Line: You're Not Powerless

Even though you can’t control the ups and downs of the economy, you can take steps to set yourself up for success. The key is working with someone who understands both your needs and the current market.

I’m one of the few A.I. Certified Agents in the world — and the only one in Summit County. That means I know ways of marketing your home that traditional agents don’t even know exist.

With over 40 years of local expertise and cutting-edge tools at my fingertips, I can help you navigate these uncertain times with clarity and confidence.

Let’s connect and put the power of intelligent marketing and deep local knowledge to work for you.

Phone: (970) 390-3711

Email: kim@kimobert.com

Website: www.kimobert.com

See what A.I. can do for the sale of your home.

|

or another way